Adapt and thrive in a rapidly changing electronic market

No Pain. Significant Gain. Drive intelligent decision-making with CQG Algos.

Market participants looking to execute large volumes of orders naturally want the best price available in their market. But this can be nebulous: Do you achieve the best price by aggressively paying up for an immediate fill or by working the order over time? At the risk of the market slipping away, either is an option, but there is a better solution.

CQG Algos. Built on new technology and tools for best execution.

Challenge

Liquidity Risk

- The futures markets' Central Limit Order Book structure creates slippage costs.

- Executing a sufficiently large order at a fair price is often impossible. Placing large passive orders on the best bid or offer is cost-prohibitive, as liquidity often disappears as a result.

- It's hard to balance the uncertainty of working an order over time versus paying a liquidity premium for immediate execution.

Solution

CQG Algos provide optimal execution

- Our CQG Algo platform reduces implicit trading costs

- Each algorithm is built to track or beat benchmarks with specific implementations dedicated to in-depth analysis of microstructure, resulting in more passive fills.

- The platform employs a collocated low-latency algo engine.

- Algos react to real-time market data in microseconds, leveling the playing field with the world's most sophisticated market-making firms.

CQG Algo Models

A new framework for fast execution

Economic

Economic Models mathematically optimize execution risk through short-term volatility, drift indicators, options-implied volatility, and statistical analysis.

Impact

The Market By Order Impact Model assures passive child orders are incognito and aggressive child orders maximize hit ratios.

The Percent of Volume Impact Model provides guidance to make sure you don't exceed a particular share of the total market.

Payup

The Payup Model comprises several modes: Simple Size-based, Order Imbalance, Fair-Queue, and Theo-Queue. These modes reduce implicit trading costs while maximizing spread capture.

Get to know the CQG Algo lineup

Arrival Price - Time is Money

Simulation Results - Detailed Analytics

Arrival Price uses short-term volatility and "drift signals" as well as market-implied volatility to execute within a risk-optimized time horizon using slippage expectations defined by the trader.

AI Optimized Arrival Price

Simulation Results - Detailed Analytics

Arrival AI uses measures of short-term volatility, liquidity, and drift signals to execute within a risk-optimized time horizon. Each child slice uses our proprietary AI Model to predict whether to aggress or remain passive.

VWAP - Trade the Market

Simulation Results - Detailed Analytics

VWAP (Volume-Weighted Average Price) uses a historical N day volume distribution, or a stochastic distribution augmented by short-term and implied volatility.

TWAP - Trade over Time

TWAP (Time-Weighted Average Price) uses a Standard or Randomized [order] sizing function that can optionally use Market By Order [instructions?] to create inconspicuous slices.

Icebergs - Trade Incognito

Random Iceberg*, Stop Limit Iceberg, Stop Limit Sniper**, Sniper

*An iceberg is an order to buy or sell a large quantity by breaking it up into several smaller orders [for better market anonymity?].

** [Sniper trading involves waiting to sell when there is panic buying or waiting to buy when sellers are panicking.]

PayUp - Work an Order

Simple "with-a-tick" or more complex order imbalance measures.

Spreader - Leg Into a Spread

Latency matters! Use our ultra-low latency spreader for multi-leg Treasury, Energy, Equity or Agricultural spreads.

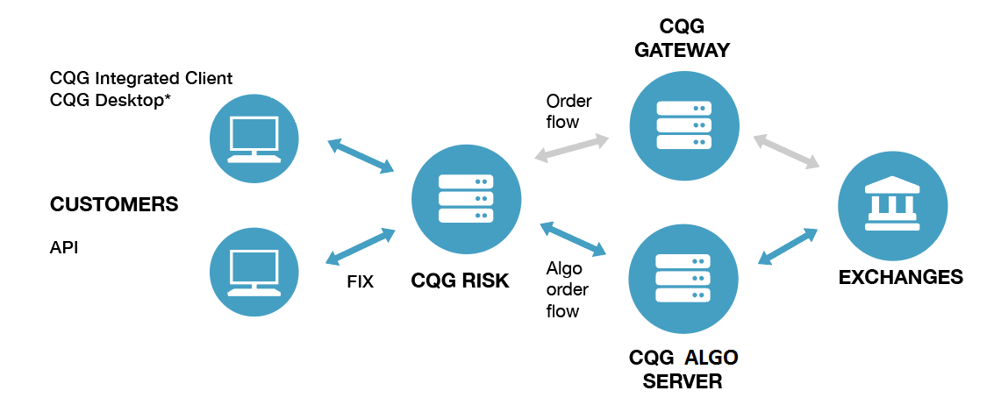

How CQG Algos Work

The kind of fast you can feel

CQG Algos deliver high-quality fills with the goal of reducing implicit trading costs involved in accumulating a derivatives position. The platform employs a collocated low-latency algo engine that reacts in microseconds to changing market conditions for optimal management of child orders.

CQG Algos benefit from better queue position in First In, First Out (FIFO) markets through low-latency execution as well as lightning-fast analysis of Market By Order (MBO) books.

Each algorithm is built on sound macro-analytical precepts with specific implementations dedicated to in-depth analysis of the current market microstructure as well as high-level statistical analysis.

Algo Order types are available by appropriate market group: Outright Futures, Futures Spreads, Options and Outright Options.